Why Benchmarks Win

A structural explanation for why benchmark assets outperform in the long-run, and why capital concentrates there.

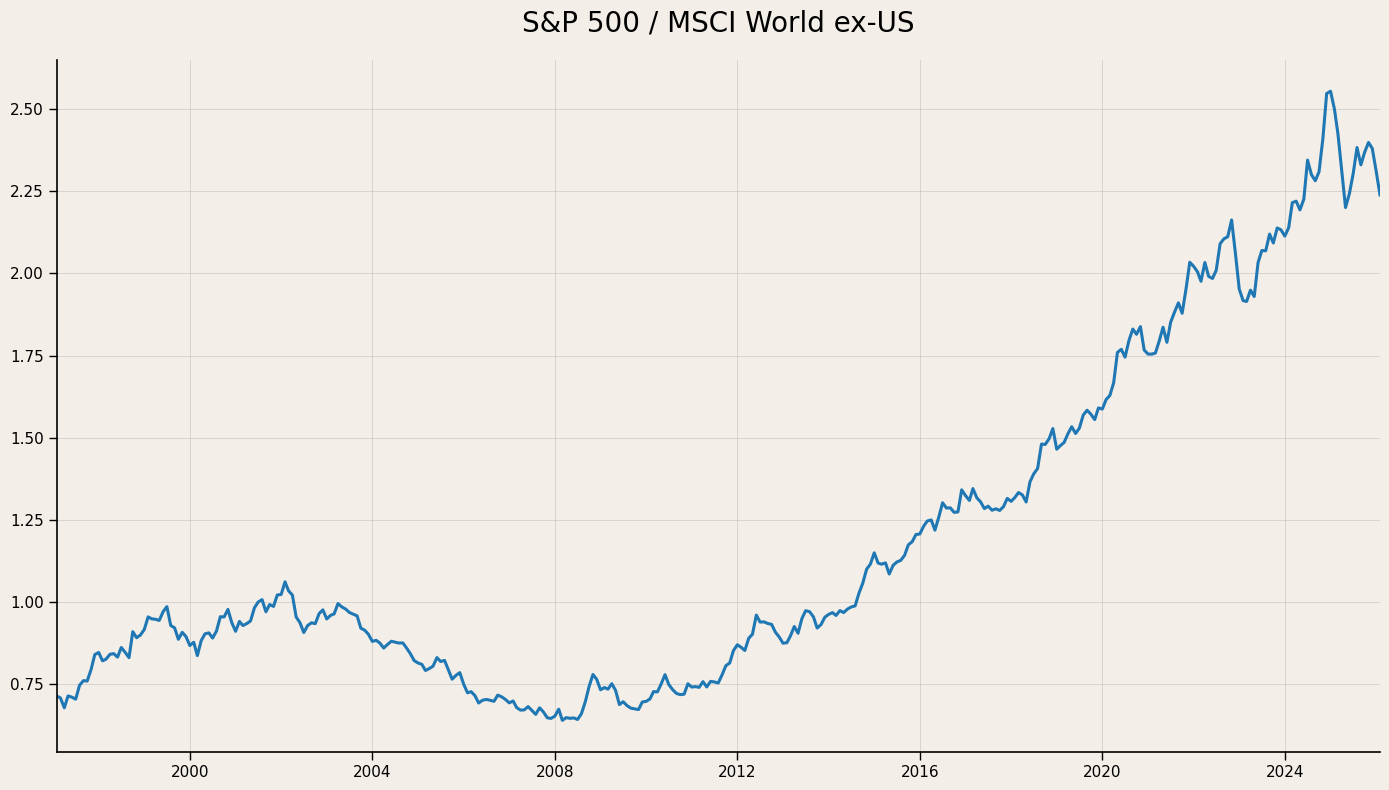

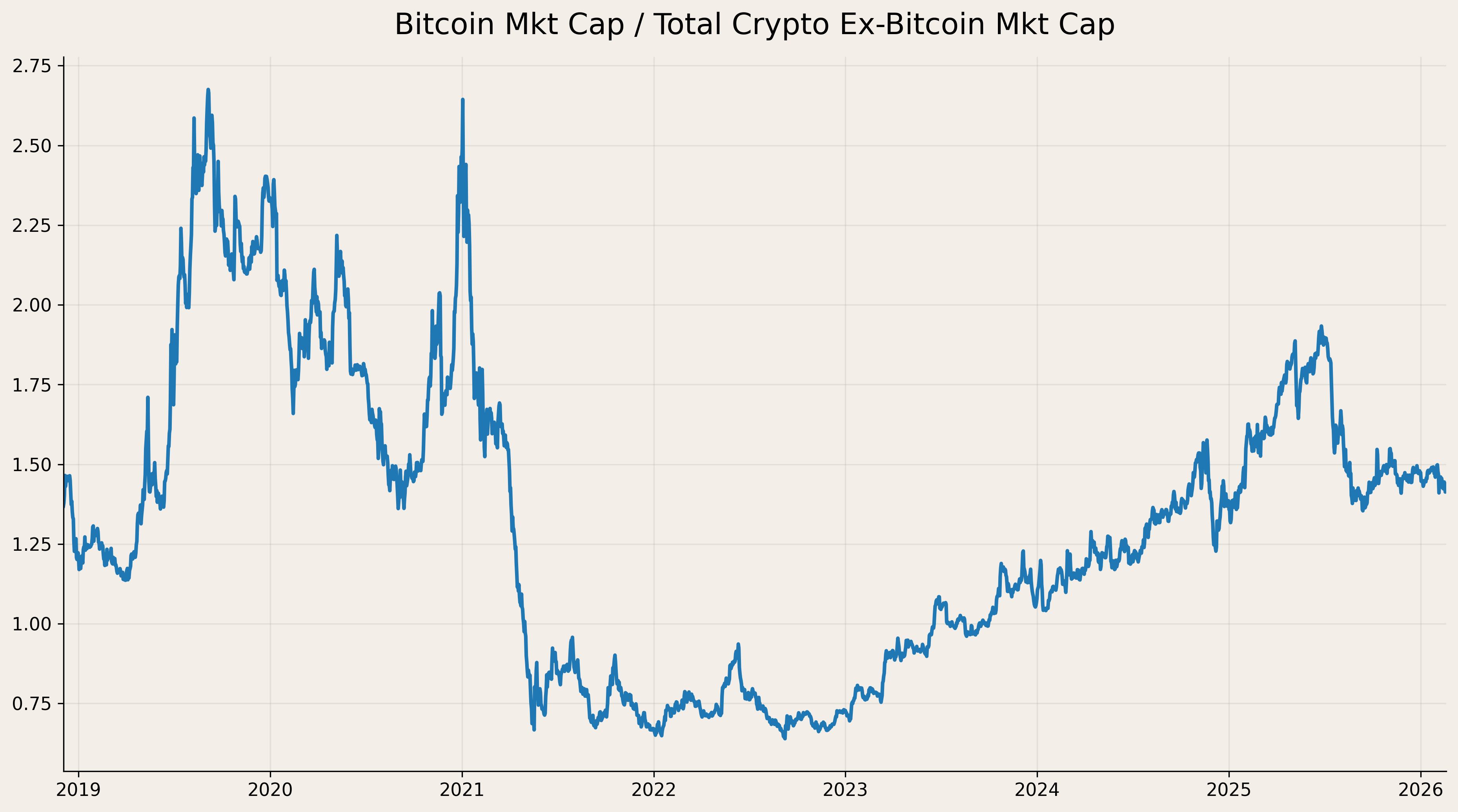

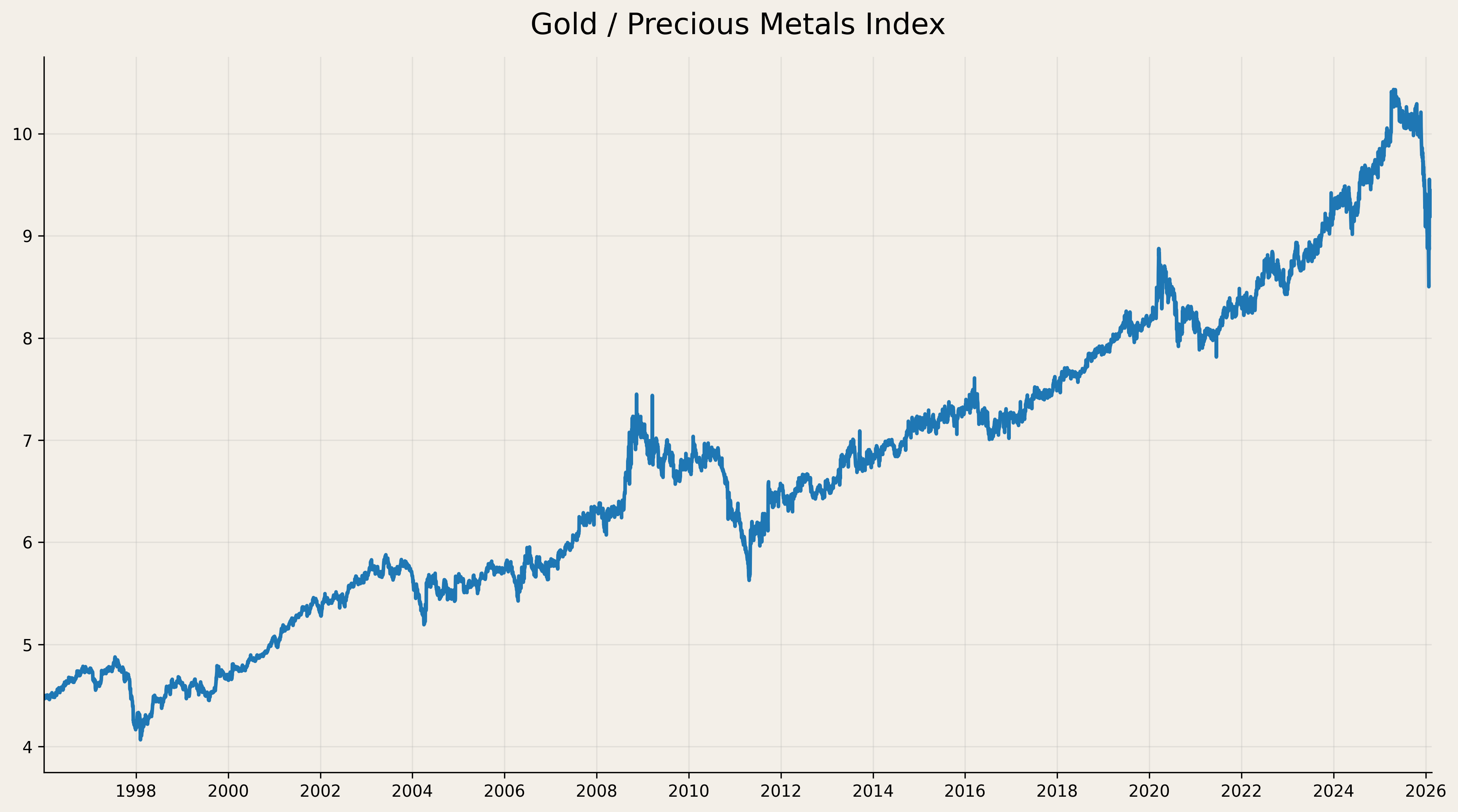

Investors are always searching for the next unicorn, the next frontier market, the next Bitcoin. And yet, over time, capital tends to return to the same places. Since 2009, the S&P 500 has outperformed the MSCI World. Gold has, for centuries, retained its role as the monetary reserve asset of last resort. Bitcoin remains the anchor of the crypto ecosystem.

Over long horizons, performance concentrates in assets that occupy the structural centre of their respective systems. The relevant question is therefore not which asset may temporarily outperform, but why the benchmark asset so often delivers the most durable risk-adjusted returns.

The answer lies in structural centrality. Assets at the core benefit from embedded demand, deeper liquidity and lower displacement risk. Peripheral alternatives may offer cyclical upside, but they carry a higher probability of obsolescence, illiquidity or structural loss of capital.

Assets such as the S&P 500, gold and Bitcoin function as global reference points within their ecosystems. They anchor pricing, flows and performance measurement. Their benchmark status rests on, among others, three key properties: flow concentration, survival across regimes and asymmetric transmission.

Flow concentration

Benchmarks are embedded in mandates, risk models and performance evaluation frameworks. Passive vehicles replicate them mechanically, derivatives markets are deepest around them, and hedging activity is structured through them. Investors seeking liquidity, scalability and minimal tracking error therefore gravitate toward the benchmark first. Over time, this institutional framework becomes self-reinforcing: performance attracts flows, flows increase weight, and greater weight further entrenches benchmark status. In that sense, benchmark centrality does not merely reflect past dominance but rather it helps to sustain it.

The S&P 500 illustrates this clearly. Broad, low-cost S&P 500 replication vehicles reached scale well before comparable MSCI World trackers. Early benchmark flows therefore concentrated in the S&P 500. As US equities subsequently outperformed, their weight within the MSCI World Index increased mechanically. A larger US weight within global indices in turn directed a greater share of passive allocation back toward US equities. First-mover advantage and relative performance reinforced one another.

Survival Across Regimes

Assets at the structural core of a system endure repeated regime shifts without losing relevance. They survive crises, policy transitions, technological cycles and speculative manias that eliminate peripheral competitors. The S&P 500 has absorbed wars, inflation shocks, banking crises and multiple sector rotations while continuously reconstituting itself around the dominant firms of each era. Gold has persisted across monetary regimes, from the classical gold standard to Bretton Woods to fiat systems, retaining its role as a reserve asset and collateral anchor. Bitcoin has survived successive boom-and-bust cycles that extinguished large segments of the broader crypto ecosystem, yet each cycle has reinforced its relative dominance.

Asymmetric Transmission

Benchmarks also function as the marginal price-setters within their systems. A 1% move in the S&P 500 transmits materially into major European and Japanese indices for example, with cross-market betas rising during stress. The reverse transmission is considerably weaker. Shocks originating in the core propagate outward; shocks in the periphery rarely reprice the centre. Gold anchors relative pricing across the precious metals complex. Bitcoin anchors liquidity and sentiment within crypto.

These benchmark characteristics are not unique to financial markets. In other ecosystems, value and liquidity similarly concentrate in the reference asset. Within collectible markets, flagship items such as first-edition Charizard cards often trade at a persistent premium and exhibit greater price resilience than comparable cards. In art, capital clusters around blue-chip names whose works function as the benchmark for the category. In prime real estate, global capital gravitates toward a small number of cities. The benchmark asset becomes the focal point for valuation, trading and capital allocation, and that focal status compounds over time.

Benchmark dominance reflects embedded flows, survival across regimes and asymmetric transmission. Peripheral assets may outperform cyclically, but over long horizons capital concentrates where liquidity is deepest and displacement risk is lowest. Accordingly, benchmarks offer structurally superior risk-adjusted returns.

If you enjoyed this article and found it insightful, subscribe for free below.

Interesting chart on gold… wonder if it’ll keep outperforming other precious metals like this or some point revert