Tesla: Driving Without Wheels

At a $1.25 trillion market cap, only 12% of Tesla's value comes from making cars. The rest is a bet on Robotaxi, Self-Driving Subscriptions, and Optimus — all of which have yet to prove themselves.

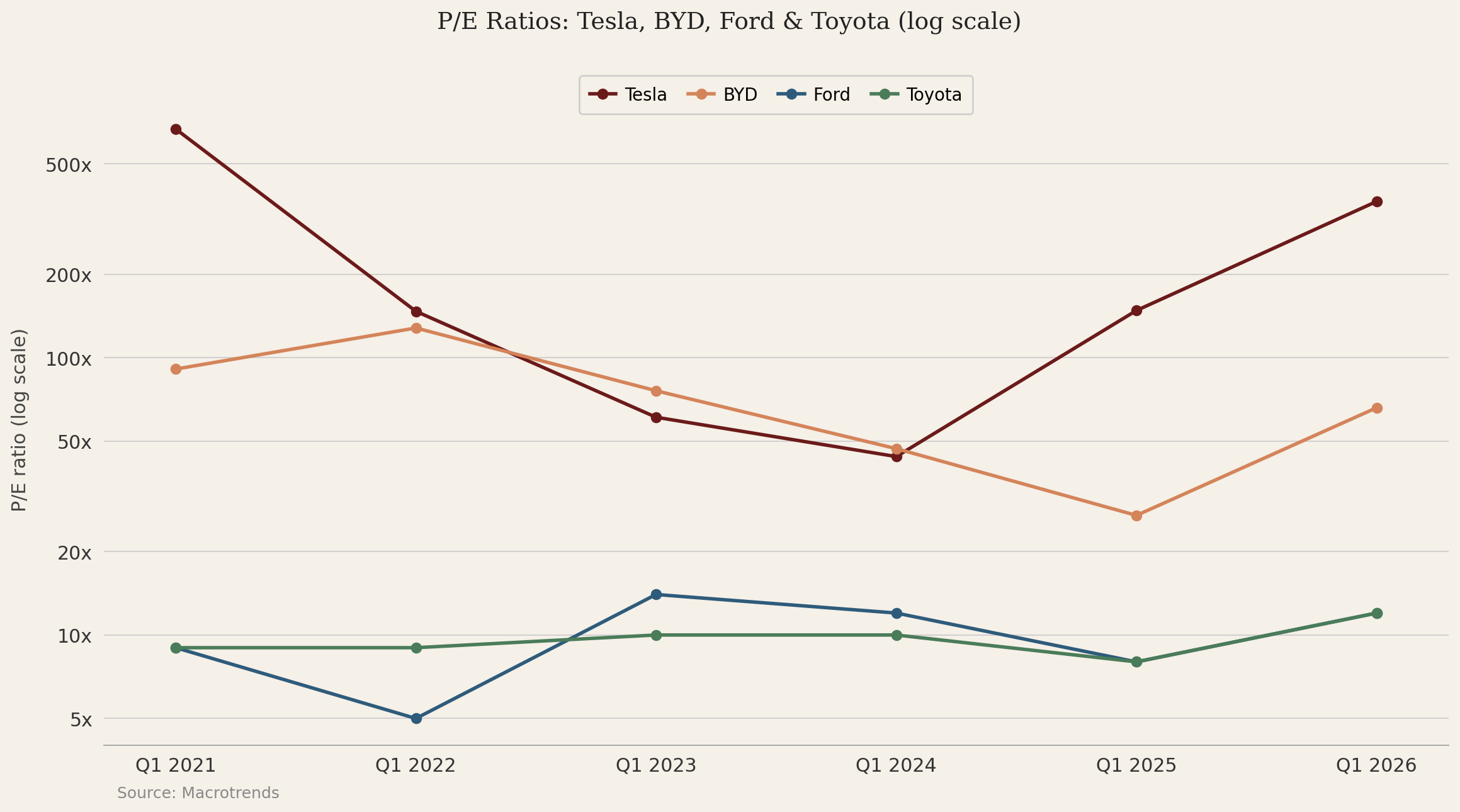

Sometimes companies are fairly valued, sometimes they are not. If you were shown a company with a Price to Earnings (P/E) ratio of 370, you would probably say it’s expensive. Whether this is justified requires us to delve deeper.

Tesla, the company well known for making electric vehicles, is one such company with a P/E of 370. This puts it as one of the top S&P 500 companies by P/E ratios. Even against high-growth US tech stocks — Nvidia, Apple, Google — it screens high. BYD is the closest automotive comparison, and that trades at a fraction of Tesla’s multiple. From the chart below, it’s clear that P/E ratios of traditional car manufacturers are vastly different. A simple glance would suggest that EV manufacturers trade at a 10x premium. What stands out most, however, is the divergence between Tesla’s and BYD’s P/E ratios over the past two years. At a ~$1.25 trillion market cap, investors are largely paying for business units beyond car manufacturing.

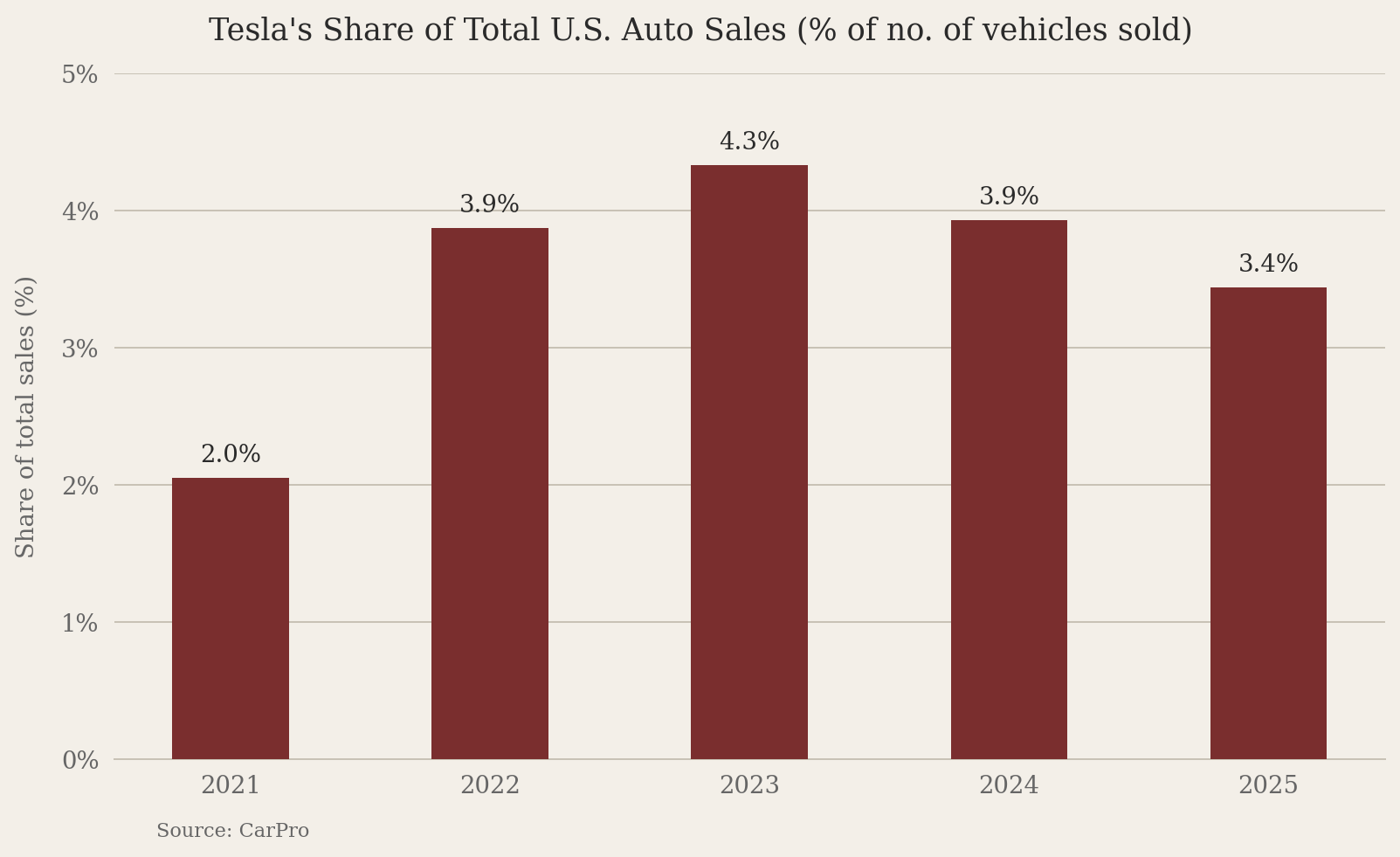

Bank of America’s sum-of-the-parts model assigns Tesla’s core automotive business 12% of its total implied value. At the current market cap, that is roughly $150 billion. For context, GM and Ford’s market caps are $67 and $47 billion respectively. Meanwhile Toyota — the world’s largest car manufacturer by volume, with total revenues more than four times Tesla’s entire automotive segment — is valued at approximately $275 billion. Tesla’s U.S. market share peaked at 4.3% in 2023 and has declined every year since (see chart below), while BYD has overtaken it as the world’s largest battery electric vehicle manufacturer.

Policy has moved in the wrong direction too. Since Trump’s re-election, federal purchase incentives have been eliminated, EV mandates revoked, and fuel economy standards rolled back – removing a key tailwind for the industry. Leaving aside the debate over how much premium Tesla’s car business deserves, investors are not buying this stock for the cars.

Tesla’s energy generation and storage unit is the company’s strongest segment, with revenues up 27% in 2025 and gross margins of ~30% across the year. Yet BofA’s model assigns it just 6% of Tesla’s total implied value, or approximately $75 billion. This still leaves over $1 trillion in valuation that must be justified entirely by three businesses that are either pre-revenue or in early pilot phase: Robotaxi, which accounts for 45% of the implied value (~$562 billion), Full Self-Driving (FSD) subscriptions 17% (~$213 billion), and Optimus 19% (~$238 billion).

Robotaxi consists of creating a fleet of self-driving cars that work like Uber. Tesla began paid rides in Austin in June 2025 and plans to expand to seven additional U.S. cities in the first half of 2026. Revenue estimates for the upcoming years vary greatly, but consensus is that breakeven will not be reached until sometime in 2027 and even then the fleet will still be tiny compared to its valuation. Weeks before Cybercab production was due to begin, Tesla lost the engineer who built its Robotaxi software backbone — an 11-year veteran whose departure raises questions about near-term execution.

FSD is Tesla's driver-assistance software, which — once fully autonomous — would allow any Tesla vehicle to operate without human input. Tesla currently charges $99 per month following the move to subscription-only in February 2026, and had 1.1 million paid subscribers globally as of Q4 2025. That's $1.3bn in annualized revenue against a $213bn implied valuation (a 163x multiple), which implies that the subscriber base would need to grow more than tenfold just to approach a conventional tech valuation.

Optimus is the most speculative of the three. It is a humanoid robot designed initially for factory automation, with longer-term ambitions in consumer and commercial applications. Musk has said 80% of Tesla’s long-run value will come from this programme. Production has slipped to late 2026, with meaningful revenue not expected before late 2027.

If you are buying Tesla shares as an automotive investment, only 12% of the business justifies that. The rest is a bet on a tech company that has yet to prove itself, and at the current valuation risks are tilted to the downside. There exists a scenario in which Robotaxi scales slower than expected, FSD monetisation disappoints, and Optimus is still years away than Musk suggests. Given that the current share price requires a smooth rollout of each business, we think Tesla will struggle to maintain its valuation.

If you enjoyed this article and found it insightful, subscribe for free below.

Agreed - horrendously overvalued. Sell the bounces.