Skating on Thin Ice

An assessment of the current US macro and market backdrop.

It has been a strong start to the year for equities, with most developed-market indices hovering around all-time highs. Gold and silver are also rallying sharply, driven by strong retail demand. Developments in rates are more mixed: the front end of the US curve is supported by a restart of technical quantitative easing, the long end is trading in a range, and the ultra-long end is drifting higher. The steepening trend observed in the US has also been playing out in Europe and the UK, although both the ECB and the BoE remain in restrictive territory. The main underperformers are Bitcoin, which has entered a bear market (to be discussed in a forthcoming article), and oil, which now faces the prospect of a significant influx of new supply.

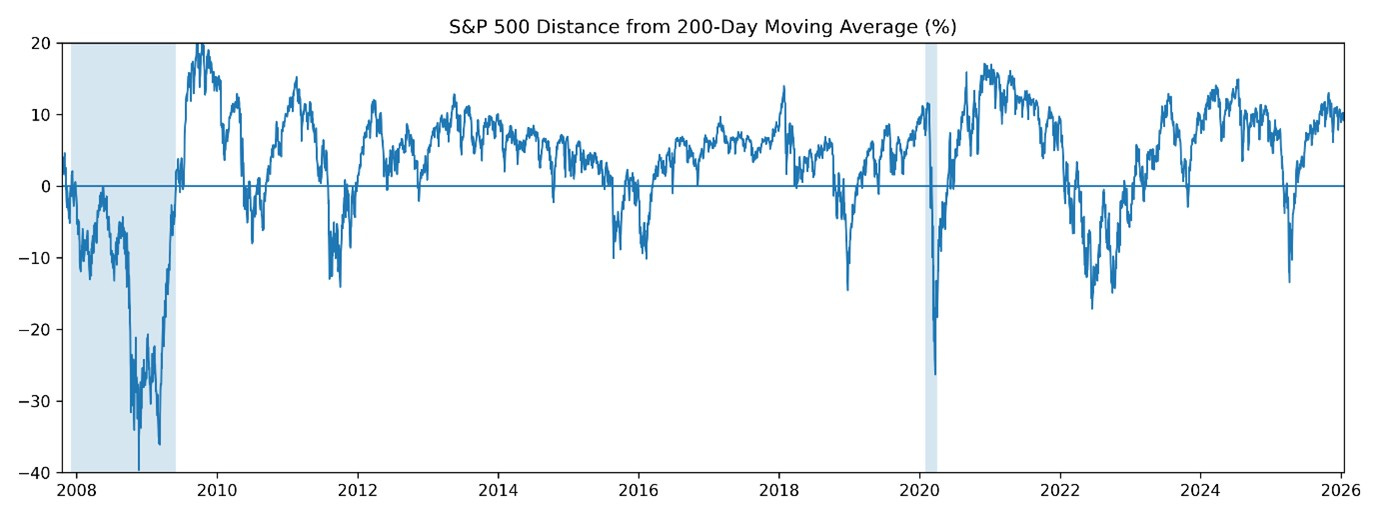

This publication focuses in greater detail on the US economy. While US equity valuations appear stretched from a technical perspective (see chart below), the fundamental backdrop remains supportive, underpinned by (i) a looser monetary policy stance from the Fed and (ii) strong economic growth driven by expansionary fiscal policy. This Goldilocks scenario, however, is akin to walking on thin ice. Should geopolitical risks, debt-sustainability concerns, or labour-market weakness materialise, a meaningful correction in equity markets may likely follow.

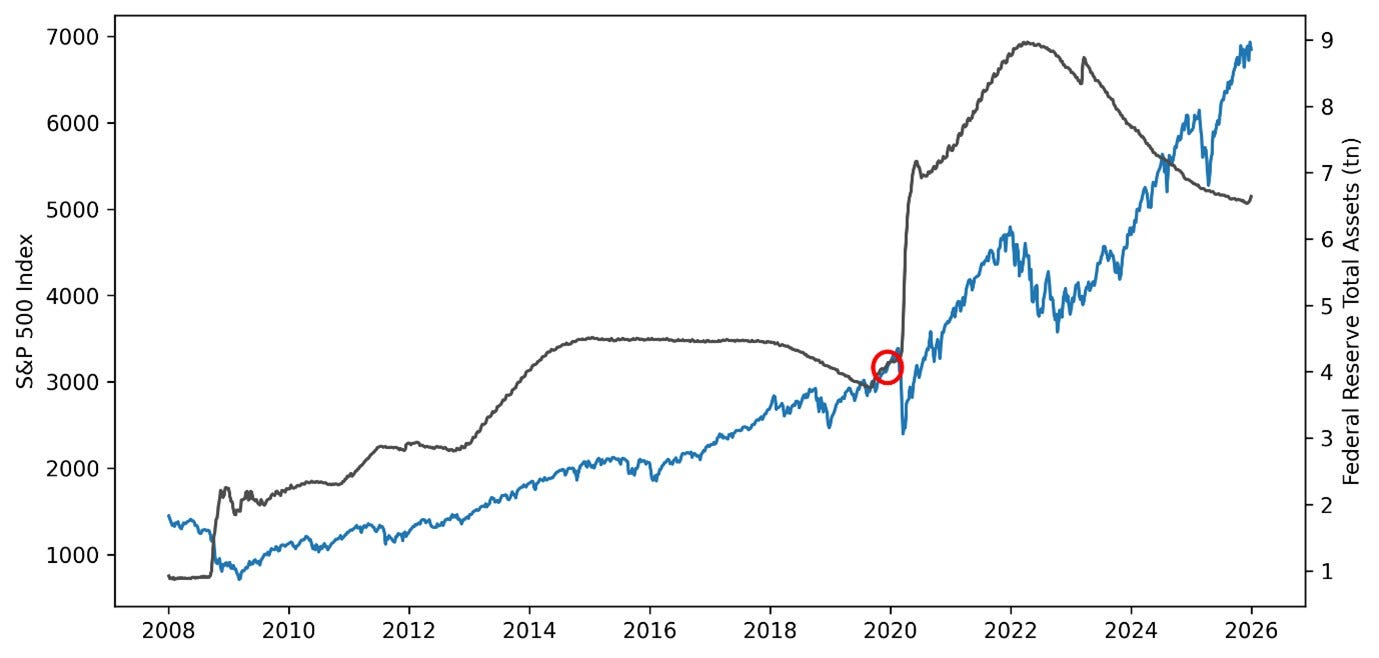

Shortly after ending quantitative tightening in November, the Fed announced on December 10 that, in order to maintain an ample supply of reserves over time, it would resume purchases of Treasury bills at a pace of USD 40bn per month until April, after which the pace will be reduced. This measure is supportive for markets, as it injects liquidity, lowers borrowing costs, and may signal reduced concern about undershooting the inflation target. Although the starting conditions differ, this episode of “technical QE” is similar in nature and scale to the programme implemented between October 2019 and March 2020, when the Fed purchased Treasury bills at a pace of USD 60bn per month to stabilise short-term funding markets (see chart below).

According to the Fed’s December projections, the US economy is expected to grow by 2.3% this year and 2.1% next year. Recent data from the Weekly Economic Index (WEI)—a composite of ten weekly economic indicators—together with services PMI data that surprised to the upside at 54.4, reinforce the narrative of a strong and resilient economy. The Congressional Budget Office estimates that 0.9% of this year’s growth will be attributable to the One Big Beautiful Bill Act (OBBBA).

A key concern, however, is the scale of additional federal borrowing implied by OBBBA, which adds pressure to Treasuries—already trading heavy—and increases rates volatility. In a paper published in November, Auerbach and Gale estimate that the debt-to-GDP ratio (defined as debt held by the public) will rise to 183% by 2054 under OBBBA as currently legislated, and to 199% if temporary tax and spending provisions are made permanent. These projections compare with a current debt-to-GDP ratio of roughly 100%, and with a pre-OBBBA CBO projection of 154% for 2054. They further estimate the fiscal gap—the permanent tax or spending adjustment required to stabilise the debt-to-GDP ratio at its current level—at approximately 3.4% of GDP if OBBBA is extended. Overall, growth generated by OBBBA appears likely to represent a short-term boost at the cost of significant long-term fiscal strain.

An additional source of concern is the growing decoupling between economic growth and a labour market that has continued to weaken. Investors had been awaiting January’s jobs report for greater clarity on labour-market conditions. The latest release, however, leaves the market broadly unchanged: monthly job creation came in below expectations (50k versus 70k), while the unemployment rate edged lower to 4.4%. Hourly earnings growth and labour-force participation were in line with expectations. Overall, the report leaves the FED in a wait-and-see position, reinforcing the view that policy is currently well calibrated.

While US equities are currently benefiting from the combination of looser monetary policy and highly expansionary fiscal policy, the equilibrium is fragile. A renewed focus on US debt sustainability, a further deterioration in labour-market conditions, and/or another escalation in geopolitical risks may likely trigger a sharp correction, pushing equity markets into a cold plunge.

If you enjoyed this article and found it insightful, subscribe for free below.

Really strong analysis here. The way you tie together liquidity injections, debt sustainability concerns, and labour-market dynamics gives readers a lot to think about. I especially like how you frame the Goldilocks scenario as “walking on thin ice” - that metaphor captures both the upside and the fragility of the current equilibrium exceptionally well. Thought-provoking and timely work.

Interesting. Still heavy in gold, will keep there until get some clarity.