Resilient Markets, Concentrated Risk and the Bid for Gold

Supportive macro conditions, elevated S&P 500 concentration and gold’s outperformance.

Since late 2022, global equities have rallied despite a sharp tightening cycle across the Fed, ECB and BoE, alongside ongoing balance-sheet normalisation. In 2024, policy rates began to move lower while quantitative tightening continued. Further easing through 2026 leaves the macro backdrop supportive for risk assets, reinforced by tight credit spreads and contained intra-EMU spreads.

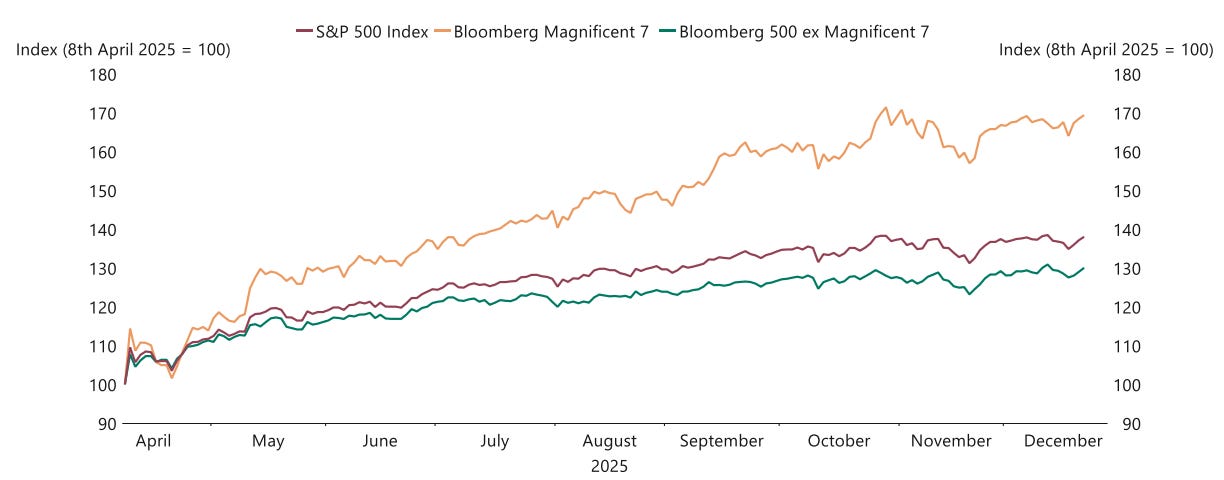

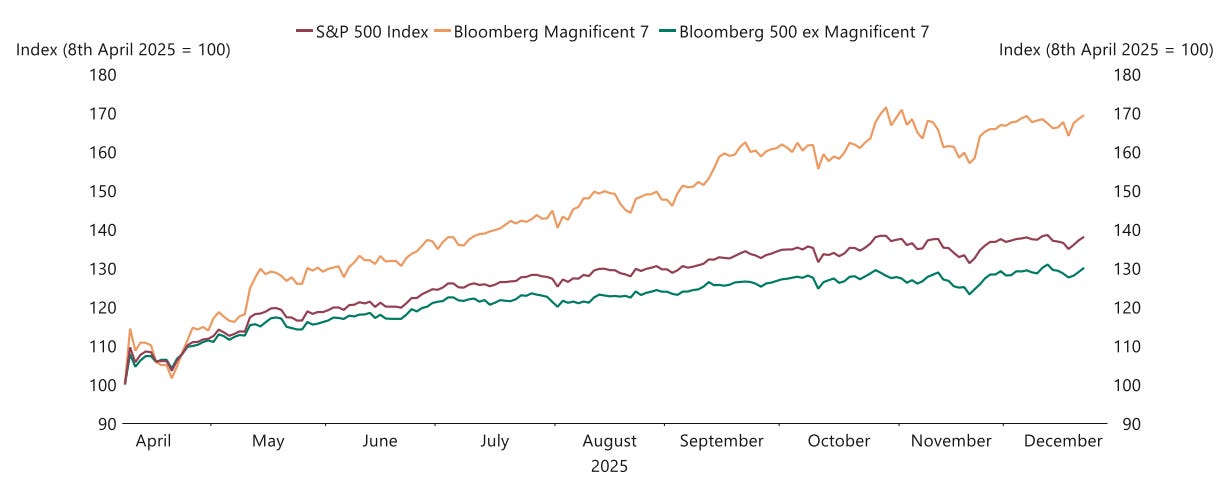

Performance in the S&P 500 has been heavily concentrated in the Magnificent Seven, meaning index returns are increasingly driven by a small number of mega-cap technology stocks. While the S&P 500 remains near record highs, gold’s relative outperformance reflects continued demand for protection against concentration risk, geopolitical uncertainty and risk-off episodes – a dynamic that can persist under the current regime.

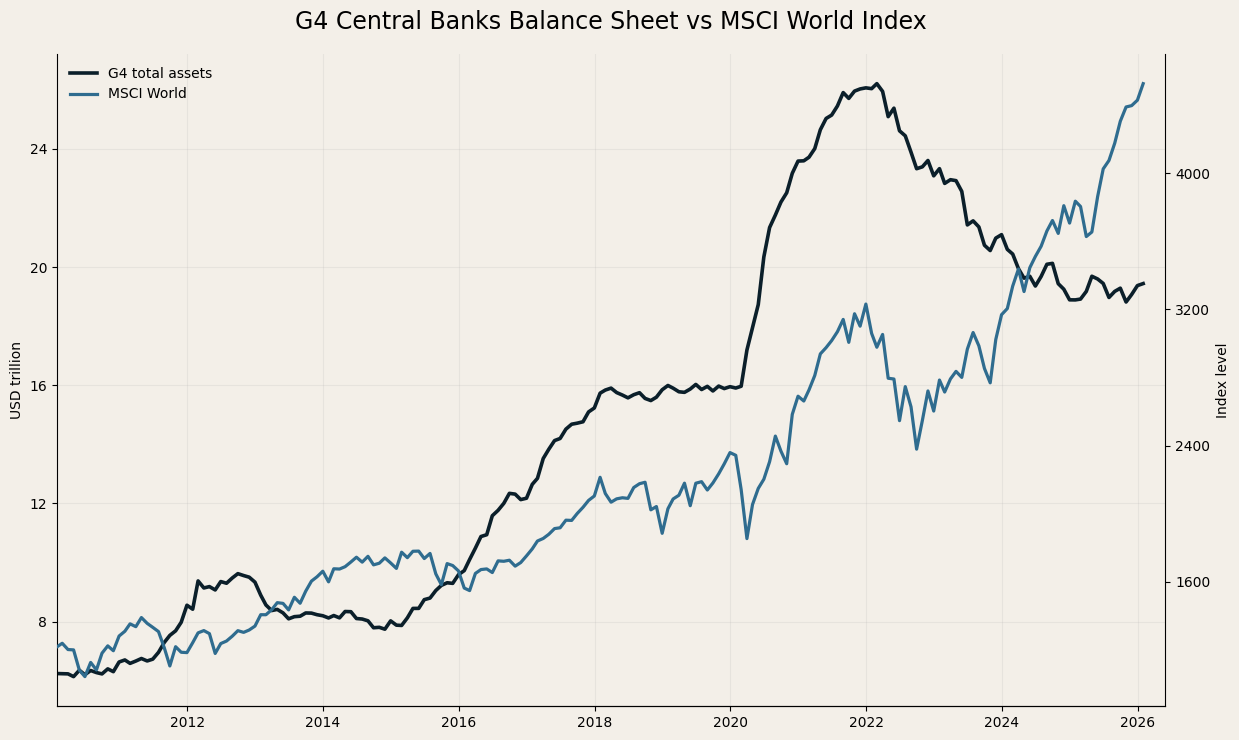

Balance-Sheet Normalisation, Continued Equity Strength

For years, global equities tracked the expansion of G4 central-bank balance sheets. That relationship weakened after late 2022. Balance sheets continued to normalise, yet risk assets recovered and advanced.

Forward earnings expectations stabilised. Excess liquidity remained elevated. GDP growth and labour markets proved resilient. AI-driven enthusiasm concentrated growth expectations in a narrow group of large firms, sustaining MSCI World performance, largely driven by US equities, despite tighter policy.

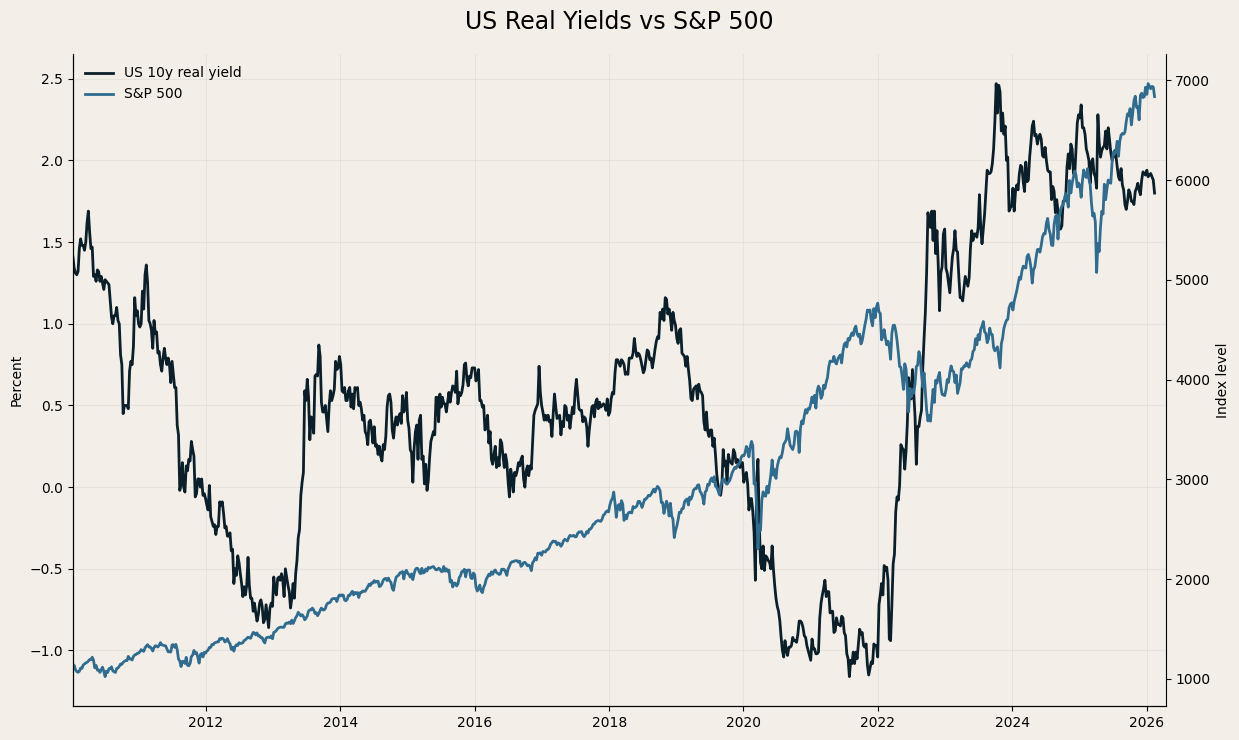

Equities in a Higher Real-Rate Regime

US real yields rose from roughly –1% in 2021 to 2.5% in 2023 before easing toward 1.8%. Historically, such a repricing would have imposed a sustained headwind for valuations. For most of 2022, it did.

The subsequent equity recovery indicates markets adjusted to a higher real-rate regime. With real yields now easing, US equities face a less demanding backdrop. To the extent the decline reflects improved inflation dynamics rather than weaker activity, it should remain supportive for valuations.

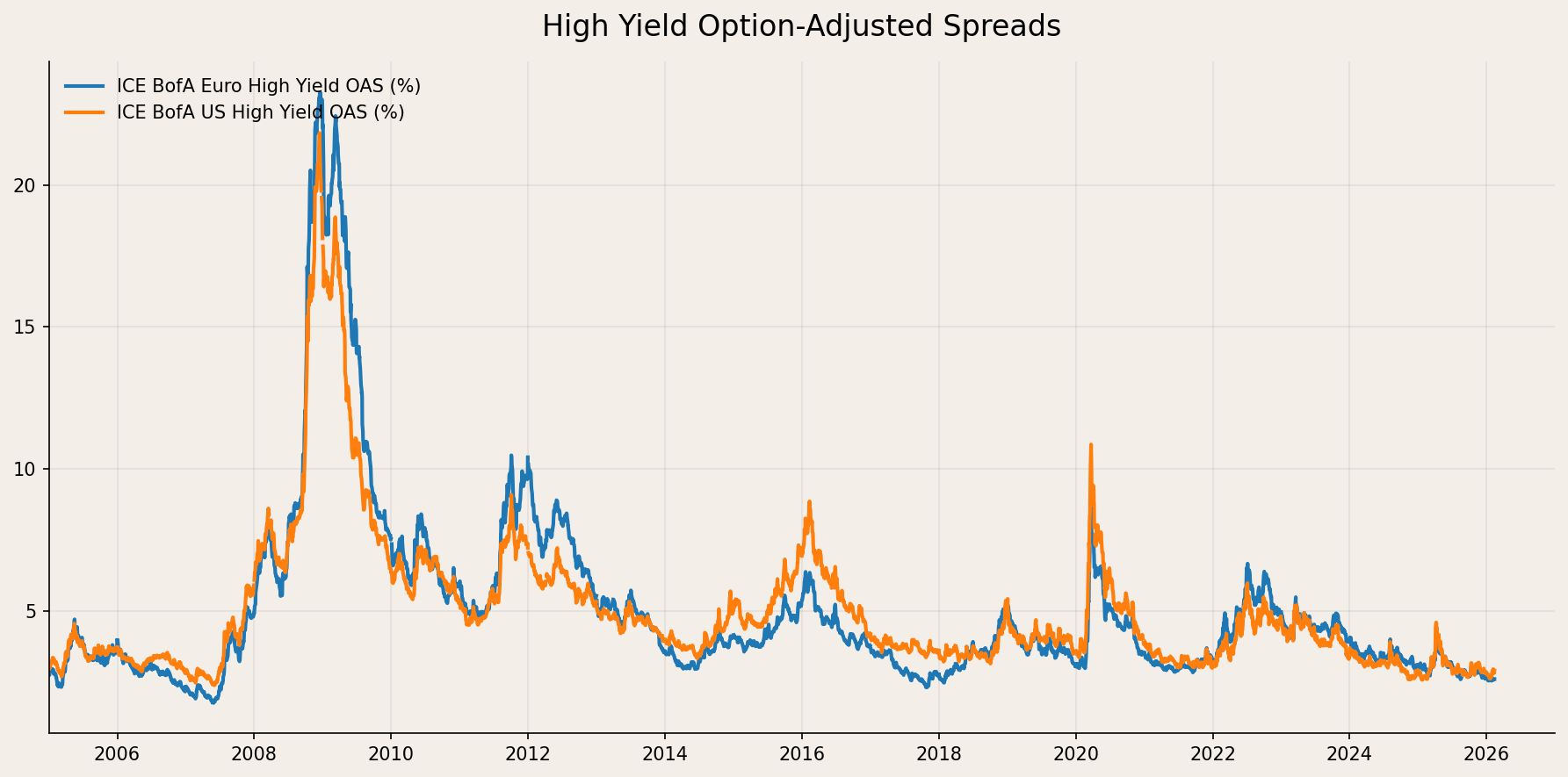

Credit Risk Premia Remain Contained

High-yield spreads signal no acute financial strain. Despite the sharp rate repricing since 2022, credit risk premia remain contained by historical standards. Episodes of volatility have followed geopolitical or policy headlines rather than a sustained deterioration in growth or funding conditions. Default expectations are limited, and markets are not pricing material funding stress in the near term.

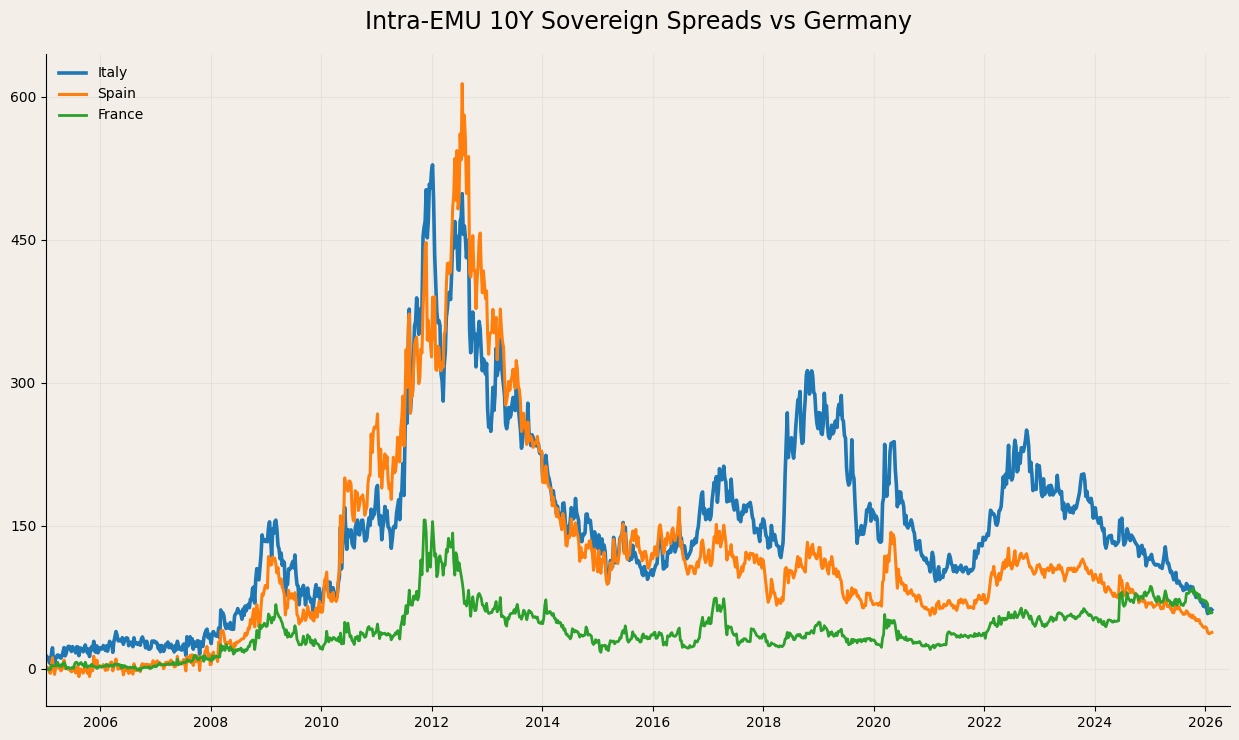

Intra-EMU Fragmentation Risk Remains Limited

Despite French political uncertainty, QT, and tariff-related tensions, intra-EMU spreads have tightened. Wider moves have failed to gain traction. With inflation close to target and limited political disruption, the direction of travel continues to favour tighter spreads.

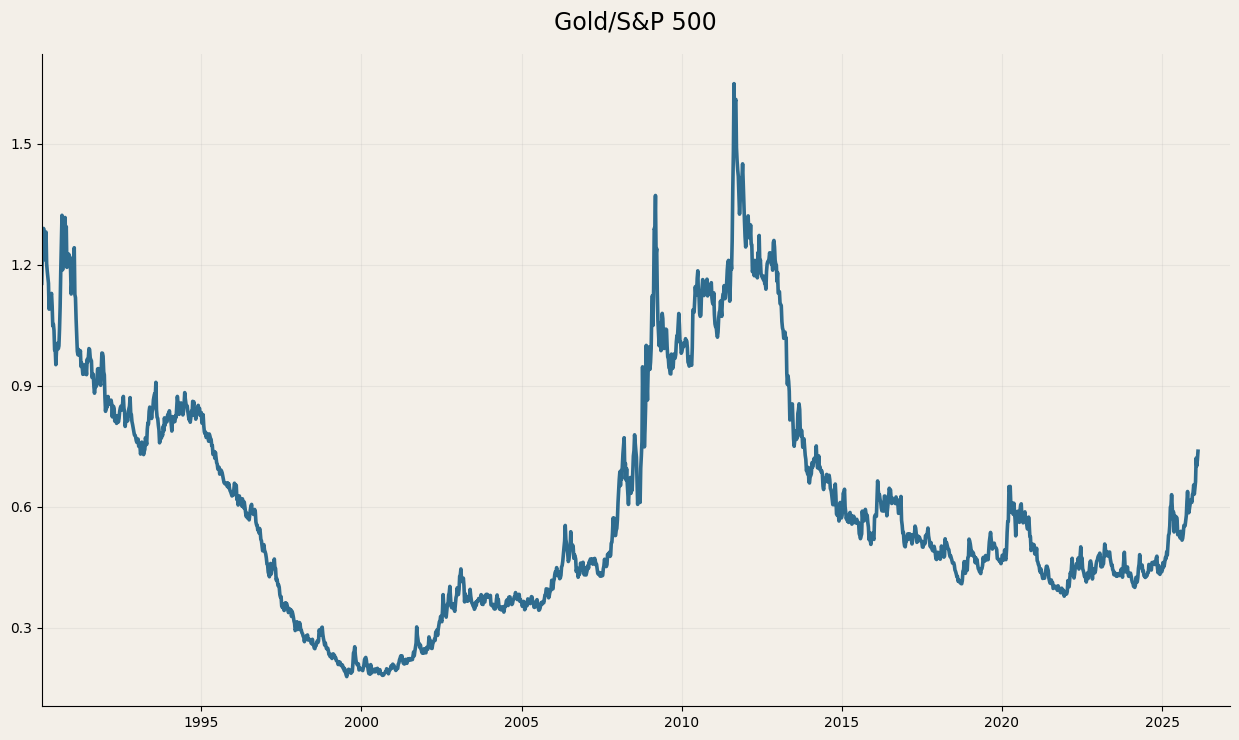

Gold’s Relative Outperformance

Gold continues to outperform relative to the S&P 500 even as indices hover near record highs. This is consistent with stretched equity valuations, debt sustainability concerns, geopolitical risk and elevated concentration in US equities. Retail flows into gold reinforce the trend.

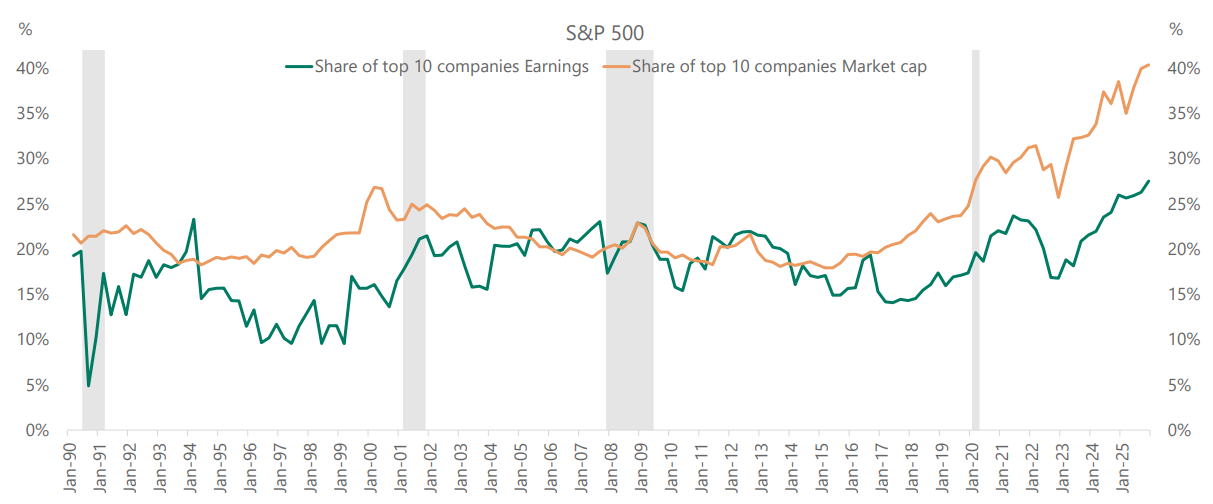

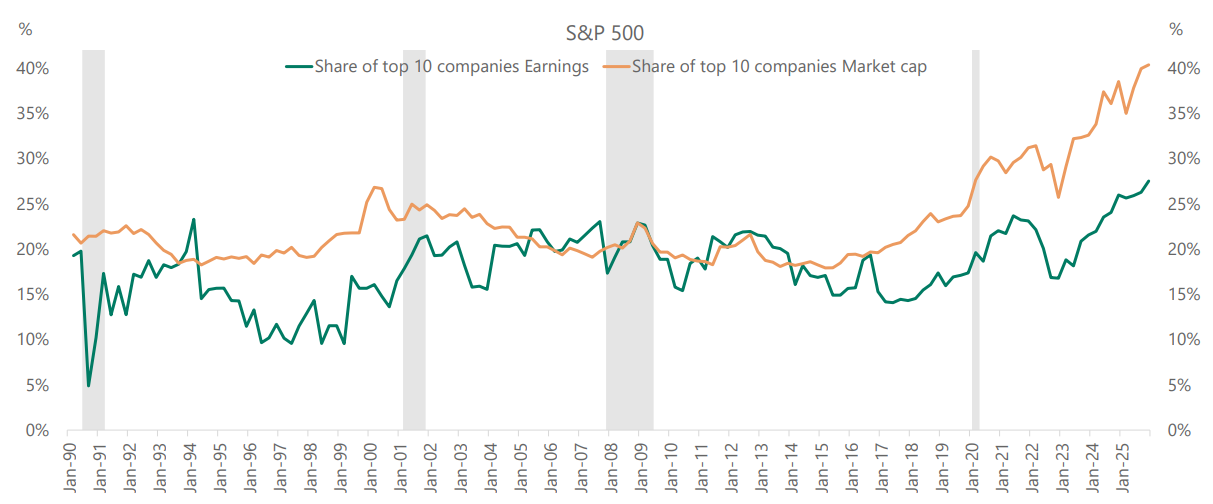

Concentration in S&P 500 Returns

Source: Apollo

The top ten companies account for roughly 40% of S&P 500 market capitalisation. The Magnificent Seven have generated a disproportionate share of returns over the past year.

In such an environment, maintaining equity exposure while adding gold becomes a coherent allocation response to concentration risk and AI-bubble concerns.

Implications

Credit and intra-EMU spreads continue to signal stability, while expansionary fiscal policy, lower real yields and strong earnings expectations support equities. At the same time, geopolitical uncertainty, elevated concentration in the S&P 500 and persistent debate around an AI bubble sustain demand for gold. In this configuration, gold’s relative outperformance against the S&P 500 can persist.

If you enjoyed this article and found it insightful, subscribe for free below.

It’s fascinating to see how AI-driven growth expectations and resilient labor markets have essentially "outrun" the traditional headwinds of quantitative tightening and higher real rates. The shift toward gold as a hedge against S&P 500 concentration risk (where 40% of cap is in just 10 names) highlights a significant structural change in how investors are seeking "defensive" exposure today.

Given that the "Magnificent Seven" concentration is largely fueled by AI expectations, do you see a specific macro catalyst—aside from a growth slowdown—that could finally force a re-correlation between central bank liquidity and these mega-cap valuations?

Great write-up. Any view on how long gold outperformance vs equities might continue? Looks like we could be in a a long run