Looking Through Chaos: Why Wars Don't Crash Markets

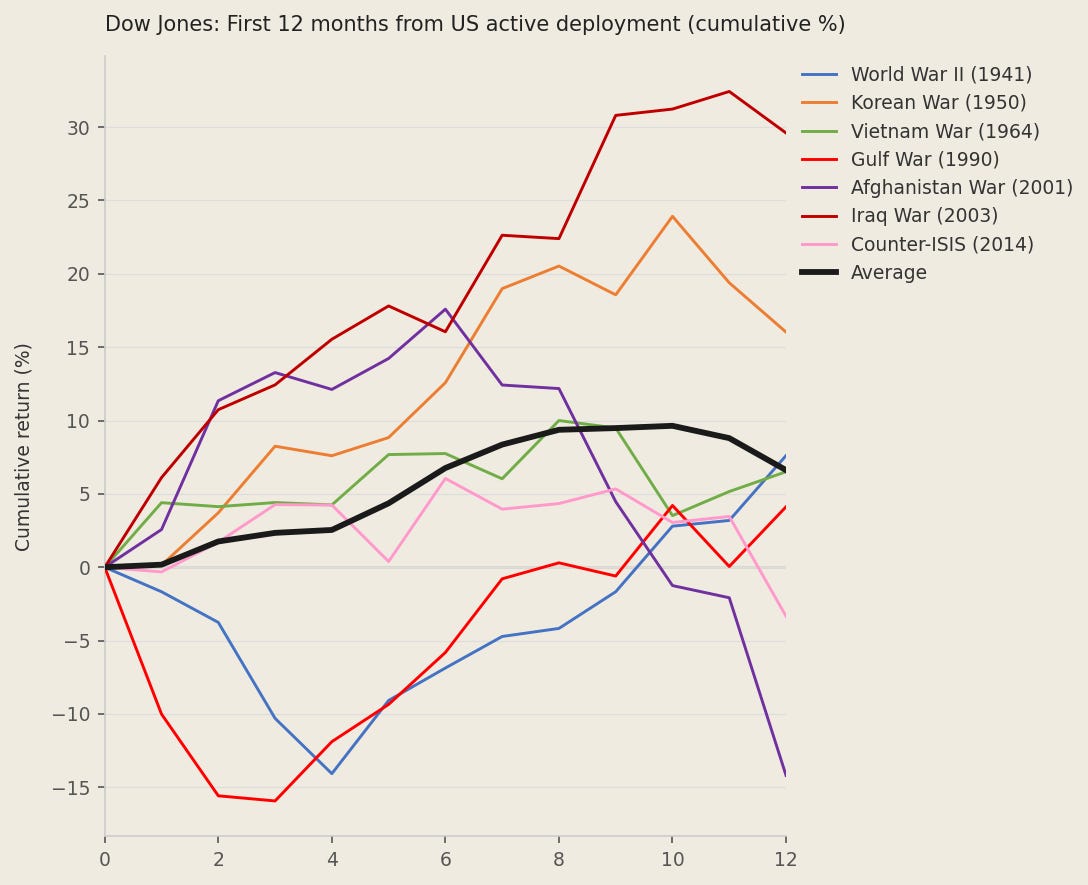

Since WWII, US stocks have averaged 6% returns in the 12 months after war breaks out.

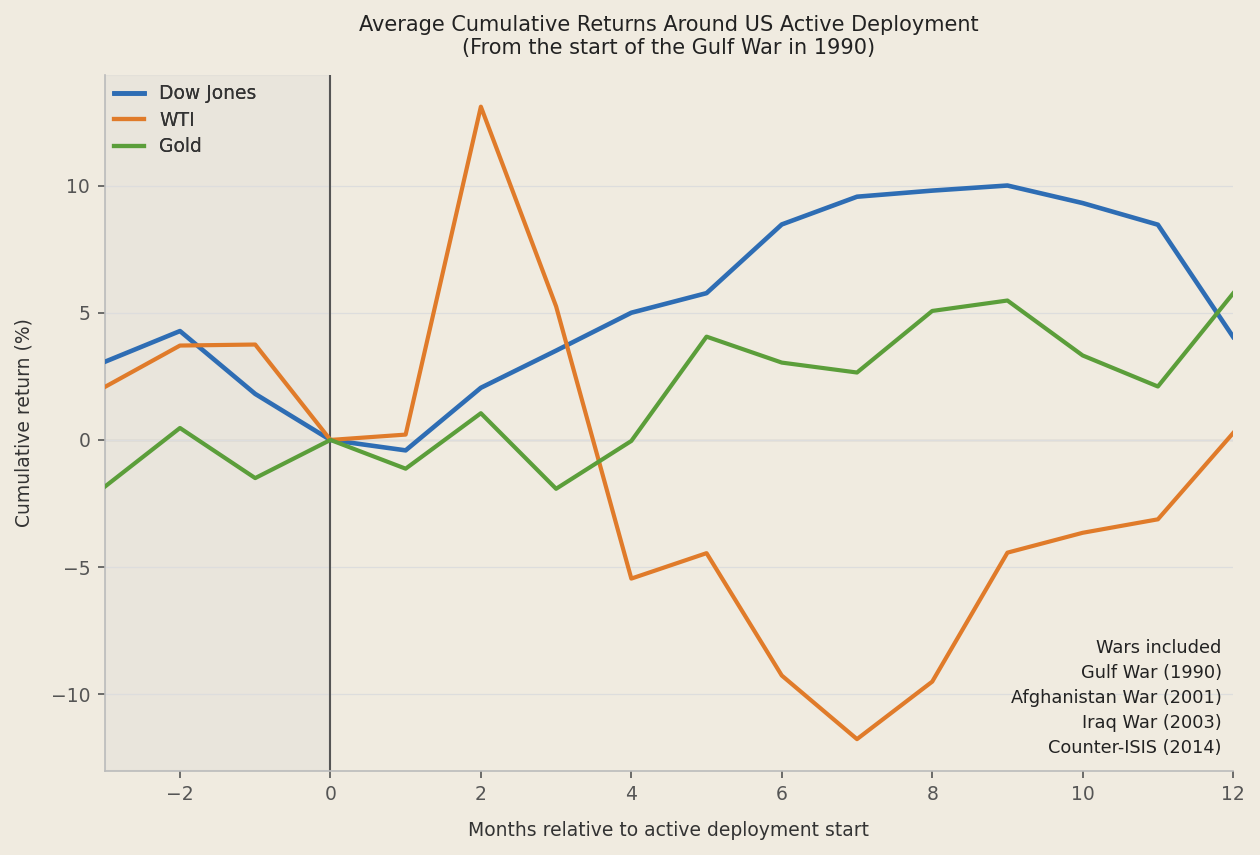

Wars. Every time they happen, people get concerned about the impact on financial markets. We all know someone who asks: should I continue buying stocks? What if the market crashes? Should I buy gold? Media outlets reporting on the first days of fighting make it sound like we’re about to enter WWIII. From a geopolitical perspective, wars can have significant consequences on the global balance of power — but from a markets perspective, this is far less so the case. US equity markets and gold, on average, both rise in the year war breaks out. WTI initially shoots higher before paring back gains to end the year roughly flat (see chart below). A combination of geographical insulation, increased defense spending, the continuous passive inflows into savings products and the dollar’s reserve status mean that US equities tend to look through war periods.

The United States has not fought a war on its own soil since the Civil War ended in 1865. This geographic insulation is arguably the single most important factor. When conflict breaks out in Europe or the Middle East, US corporate earnings, supply chains, and physical infrastructure are almost never directly affected. This contrasts sharply with European markets, which have historically exhibited far greater sensitivity to conflict. When North Korea invaded the South in June 1950, West German and broader European equity markets sold off sharply — investors were pricing in the possibility of a Soviet-backed push through Central Europe. The Dow Jones, by contrast, absorbed the shock almost immediately and was up over 16% twelve months later.

The looming risk, or outbreak of war, increases spending in the defence sector both domestically and internationally. When spending on defence increases, payrolls, capex and R&D all increase, providing support to the US economy. The Korean War rearmament programme contributed materially to the sustained post-war economic expansion. The post-9/11 buildup drove a prolonged period of elevated defence outlays. Additionally, the three world’s largest defence contractors, Lockheed Martin, Raytheon and Northrop Grumman are all American. Russia's invasion of Ukraine triggered the largest rearmament of NATO allies in a generation, with the overwhelming majority of supply coming from US-manufactured systems. The Israel-Gaza conflict reinforced this dynamic further: Israel accelerated procurement of F-35s, precision munitions and Iron Dome replenishment — almost exclusively sourced from American manufacturers — while Gulf states, rattled by Iranian proxy activity across the region, responded with a wave of US arms purchases. Saudi Arabia and the UAE together committed to tens of billions of dollars in new US defence contracts in the years following October 7th 2023. The subsequent escalation involving Iran in 2026 has cemented American defence contractors as the primary financial beneficiaries of Middle Eastern instability, as regional powers doubled down on US military systems.

Perhaps the most underappreciated reason US equities look through wars is more structural: a substantial portion of equity demand is almost entirely indifferent to geopolitics. Every month, hundreds of billions of dollars flow automatically into US equities through 401(k) contributions, pension fund allocations, and target-date funds. The institutionalisation and automation of retirement savings over the past four decades has created a recurring US equity bid that is mostly indifferent to geopolitics. This dynamic is not confined to American savers. Pension funds, sovereign wealth funds and institutional investors worldwide use US equity indices as their primary global equity benchmark, providing a consistent bid in the market.

Finally, geopolitical shocks trigger a flight to safety with the main beneficiary being the US Dollar. Although there was much talk about de-dollarisation during Trump’s second term in office, the Iran war has proven once again that, during periods of uncertainty, global investors see US markets as safest. As in the past, investors rotate out of risk assets and into dollar-denominated instruments: US Treasuries, money market funds, and ultimately US equities themselves. This dynamic was visible following the Gulf War, September 11th, and the invasion of Ukraine: in each case the dollar strengthened materially in the weeks following the shock, compressing the risk premium on US assets relative to the rest of the world. For a foreign investor holding US equities, dollar appreciation provides an additional layer of return on top of any market performance. War-driven dollar strength therefore supports US equity valuations.

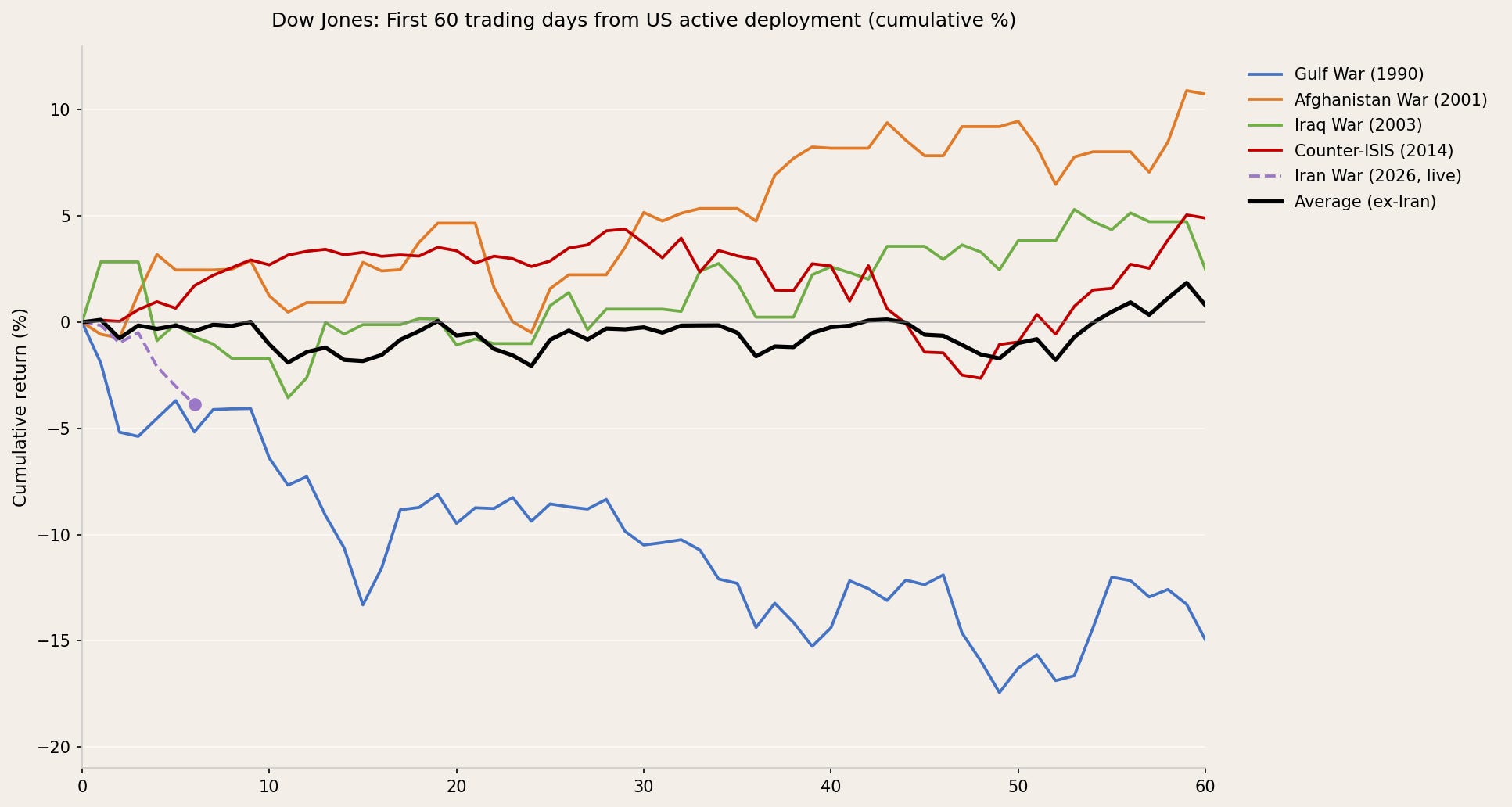

While media outlets constantly report on bombings, casualties and spark fear, markets — especially US equities — have largely looked through all this. Since WWII, US equities have, on average, returned 6% in the 12 months following US active deployment. Even in the first 60 trading days, US equity markets have, with one exception, held their ground or risen (see chart below). The US fights its wars abroad, benefits economically from the rearmament they trigger, and attracts capital when uncertainty spikes. Geography, defense spending, the dollar’s reserve status, and the continuous buying flows from passive vehicles are all supportive for US equities.

If you enjoyed this article and found it insightful, subscribe for free below.

Bounce right on time - do you think the conflict is over?