Japan Prints. Markets Price.

Japan’s macro backdrop remains constructive, rates look set to continue repricing, equity valuations appear stretched, and USDJPY holds within a range.

Despite renewed concerns around fiscal expansion and the recent sell-off in JGBs, Japan’s macroeconomic backdrop remains constructive. While rates have already repriced meaningfully, the adjustment may not yet be complete. Equities remain fundamentally supported by fiscal policy and earnings momentum, despite stretched valuations. On FX, central bank policy dynamics point to USDJPY remaining range-bound.

According to the latest Bank of Japan estimates, GDP growth is expected to reach 1.0% in 2026 and 0.8% in 2027, while core-core inflation is projected at 2.2% and 2.1% respectively. The unemployment rate continues to hover around 2.6%, underscoring persistent labour-market tightness. At the same time, the Bank of Japan is proceeding with policy normalisation—slowing JGB purchases and delivering incremental rate hikes—while Prime Minister Takaichi has pivoted decisively toward a more expansionary fiscal agenda. Recent announcements include additional spending on free education, targeted support for strategic sectors such as semiconductors and AI, a suspension of the food tax, and an increase in defence spending from 1.4% to 3% of GDP. In the snap election of 8 February, the LDP secured 316 of the 465 seats in the lower house, and 354 together with the Japan Innovation Party. The scale of the victory materially strengthens the government’s ability to implement its fiscal programme with limited parliamentary resistance.

Japanese rates have been repricing steadily over the past four years, driven by higher term premia and a slow normalisation of BoJ policy. That process has intensified more recently amid concerns over PM Takaichi’s proposed fiscal expansion. According to a study by Allianz Research, Japan’s debt-to-GDP ratio—currently around 200%—could rise to roughly 228% by 2050 if both the food-tax suspension and higher defence spending are implemented, and to over 250% if yields remain at levels implied by current forward rates. While these levels may appear elevated, Japan’s position as a net external creditor provides a medium-term stabilising channel: domestic investors can gradually rebalance away from foreign assets and towards JGBs, helping to cap upside pressure on long-end yields. That said, despite the scale of the recent sell-off, near-term risks remain skewed towards further repricing. Assuming trend growth of around 1% and inflation near 2%, a 10-year JGB yield around 3% appears broadly consistent with the macro backdrop. Additionally, given that many hedge funds have structurally short JGB basis positions (ie. long future vs cash bonds), shocks that lead to higher rates may be exacerbated by position unwinds by hedge funds. While the 30-year sector—having briefly spiked to nearly 4% before retracing to around 3.5%—should find support from real-money demand and lighter issuance, pressure in the 5- to 10-year sector is likely to intensify amid heavier supply. We may therefore see a continued flattening in 10s30s.

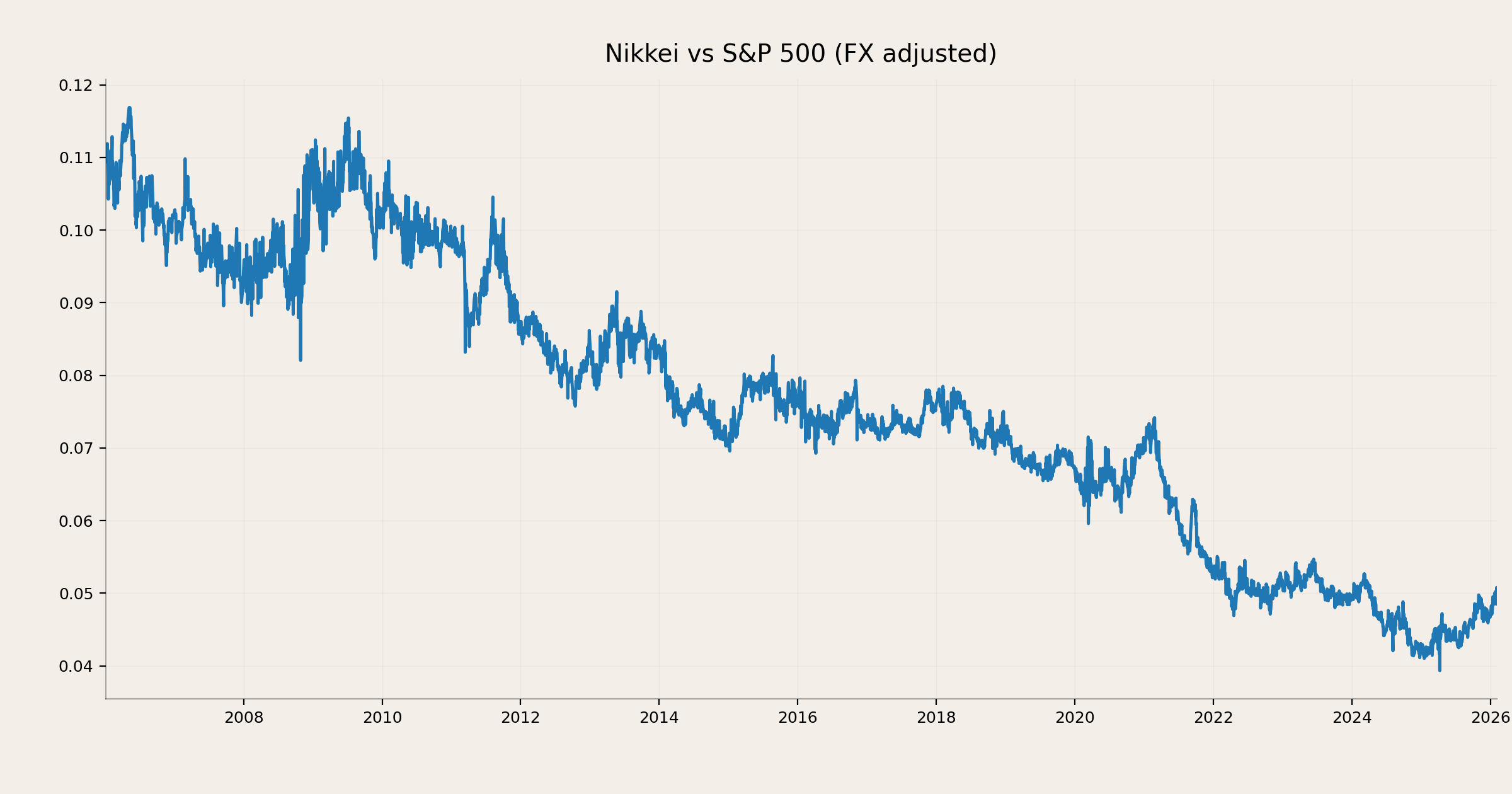

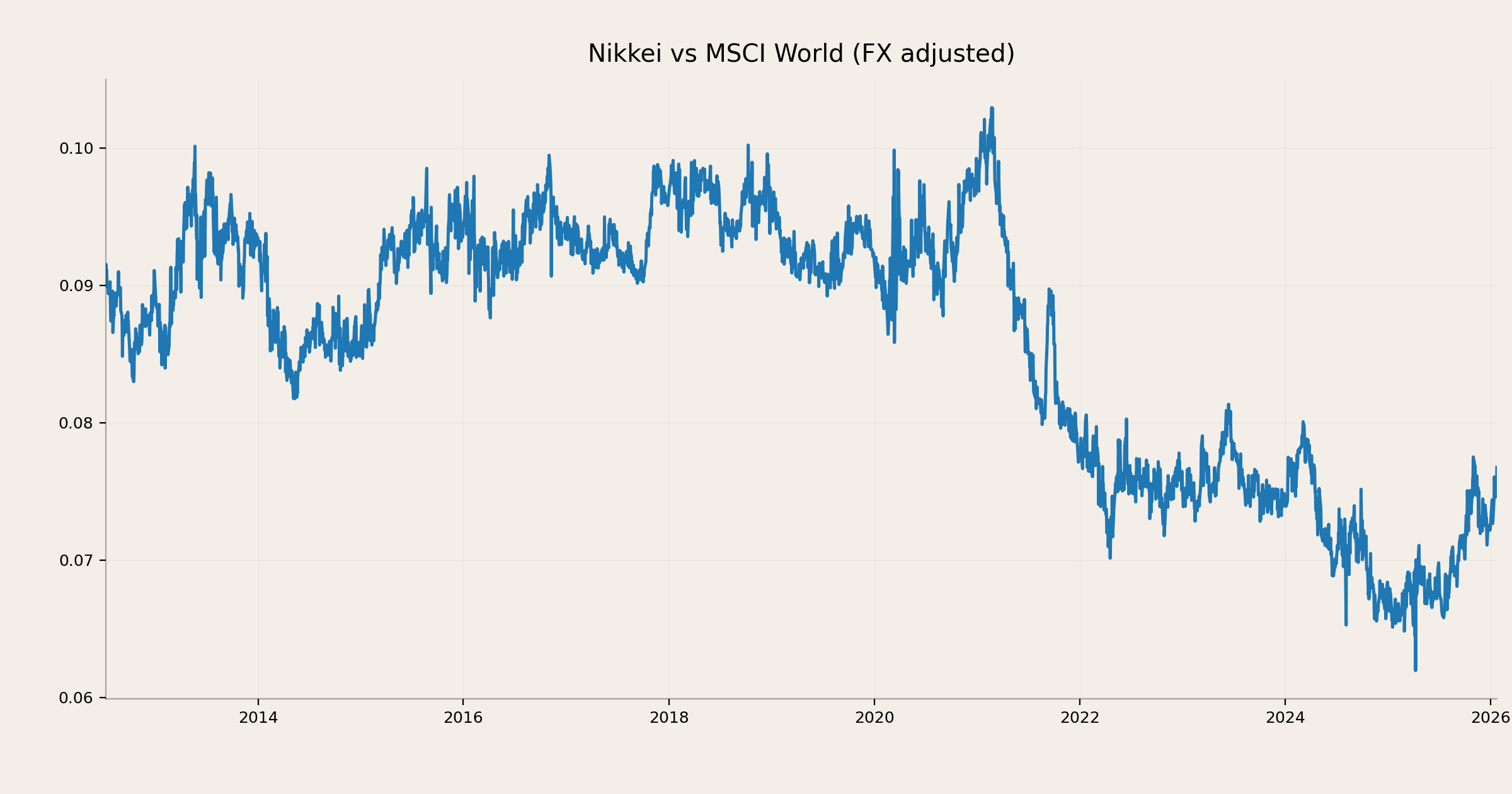

Turning to equities, Japanese stocks remain fundamentally supported by the expansionary fiscal stance, which is positive for earnings and supportive of domestic demand. Recent strength has been driven by robust earnings in AI-related firms and semiconductor companies, alongside renewed retail buying, pushing the Nikkei to fresh highs. From a technical perspective, however, valuations appear stretched. Much like in the US and other developed markets, Japanese equities look increasingly vulnerable to adverse geopolitical headlines. The Nikkei 225 is currently trading around 23% above its 200-day moving average. In relative, FX-adjusted terms, it has outperformed the S&P 500 by 22% and the MSCI World by 18% over the past year (See charts below). While this relative strength may appear bullish, the data suggest risks remain skewed to the downside, with recent performance more consistent with a temporary phase of relative outperformance.

On FX, while never officially acknowledged, USDJPY around 160 appears to represent a de facto intervention threshold for policymakers. The most recent episode of suspected intervention occurred on 23 January, when USDJPY fell sharply from around 159 to 153, potentially reflecting a coordinated effort between the BoJ and the Fed. From the BoJ’s perspective, as highlighted in the most recent Summary of Opinions, “the pass-through to prices of higher import prices caused by the yen’s depreciation has become more pronounced,” raising the risk that CPI disinflation slows or even reverses should the yen weaken further. A depreciating yen also feeds into higher term premia and expectations of a more aggressive normalisation path, exacerbating pressure on JGBs. From the Fed’s perspective, a sell-off in JGBs tends to spill over into US Treasuries, with most estimates suggesting that a 10bp move in JGB yields lifts UST yields by around 3bp. In addition, a weaker yen partially offsets the impact of the 15% tariffs imposed by the US on Japan last year. Taken together, these dynamics argue for USDJPY continuing to trade within a range, with the upper bound anchored around 160.

Overall, the outlook remains one of a constructive macro backdrop, ongoing but incomplete rates repricing, fundamentally supported—if stretched—equities, and a yen likely to remain range-bound.

If you enjoyed this article and found it insightful, subscribe for free below.

Nice and clear. Thanks for the update

time to scoop up some JGBs