Geopolitics as a Structural Driver of US–EU Rate Divergence

Geopolitical tensions risk becoming a structural driver of US–EU rate divergence, as tariffs may affect inflation and growth asymmetrically.

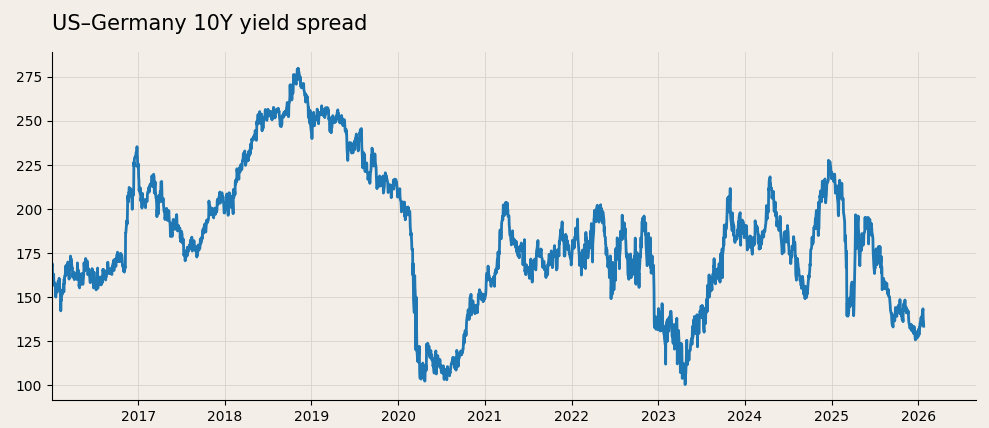

For the US, tariffs may add to inflationary pressures at a time when growth remains resilient and public borrowing is rising, constraining the Fed’s ability to ease policy and increasing the risk of a further repricing at the longer end of the curve. For Europe, by contrast, the dominant effect may be weaker growth, pushing the ECB towards a more accommodative stance as inflation is broadly under control. In this environment, geopolitical risk may no longer act as a symmetric global shock, but rather as a structural driver of rate differentials. A scenario in which the euro area gradually scales back its exposure to US Treasuries would only amplify this dynamic.

The geopolitical landscape has become increasingly fragile: Trump’s latest efforts to acquire Greenland risked turning into an open rupture with Europe. On January 17, Trump threatened new 10% trade tariffs “on any and all goods” on a number of European countries, including the UK, if these did not support his plans to take over Greenland. However, Trump’s actions towards Venezuela, followed by his stated intention to acquire Greenland, have deeply shaken European leaders and once more demonstrated how the threat of tariffs under the Trump administration is always looming.

The tariffs were initially set to take effect on February 1, rising to 25% from June if no deal were reached. In response, the EU has moved to reactivate measures previously put on hold after the July trade agreement, including $93 billion worth of retaliatory tariffs. The bloc could also activate its Anti-Coercion Instrument (ACI), which allows for restrictions on access to the EU market across trade in goods and services, foreign direct investment, financial markets, and property rights. While not currently intended, this remains an option of last resort.

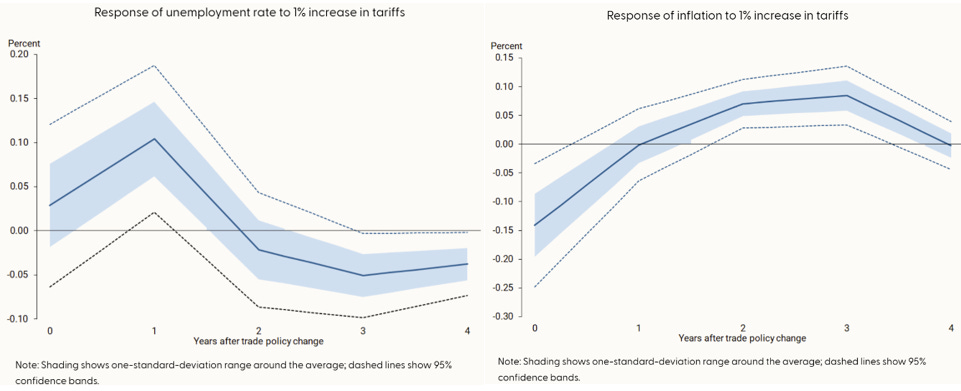

Latest economic data point to the resilience of the US economy, with household spending increasing to 0.5% m/m (0.3% previously), while both headline and core PCE came in in line with expectations at 2.8%. Although the labour market is sending mixed signals, the overall picture suggests that the Fed’s wait-and-see policy is well calibrated. At the same time, as the Fed seeks to preserve its independence, it is unlikely to cut more than what is already projected unless strictly necessary. The December dot plot shows that the Fed is expected to cut once this year, while the market is pricing in almost two cuts. A serious threat or imposition of tariffs, leading to a tariff war with the EU, may therefore lead to a market repricing: the short end may drift higher on the back of fewer expected cuts, while the long end may come under more pressure, causing a bear steepening of the curve. The moves may be exacerbated by retail or fast money investors selling US rates aggressively, as observed in April 2025. As suggested by a recent study by the San Francisco Fed, the imposition of tariffs would initially increase unemployment and decrease inflation, acting as a brake on the demand side of the economy (see charts below). Over time, the economy adjusts: unemployment returns to its original level or even declines slightly, while inflation picks up and peaks three years after the initial change in tariffs. At a time when public borrowing is increasing at worrisome levels and the Fed needs to prove its independence by not giving in to Trump’s calls for cuts, an imposition of tariffs with EU retaliation may lead to an aggressive repricing in US rates, especially at the longer end of the curve.

The ECB finds itself in a rather different position. Headline euro area CPI stands at 1.9% (with core still at 2.3%), while unemployment is at 6.3%, near historical lows. Regarding the latest threat of tariffs, ECB President Lagarde stated that this would affect euro area inflation only minimally, given that inflation is already under control. What is more concerning for the ECB is the impact on economic activity that tariffs would bring, as Governing Council member Nagel recently noted in an interview. While the ECB is currently at a neutral rate of 2%, an imposition of US tariffs may push it to loosen its monetary policy stance in order to support growth, potentially leading to a widening in US–European rates (see chart below).

In a more extreme case of tariff escalation, the EU could consider purchasing less of, or even selling, US Treasuries in retaliation. This, if it were to happen, would be gradual, but it would imply that it becomes harder for investors to absorb an increasing supply of US government debt. As pointed out by economist Erik Nielsen, the euro area alone runs a current account surplus of EUR 400–450bn per year, a large share of which is invested in US Treasuries. Following recent episodes of geopolitical tension, there is an increasing number of European policymakers and economists suggesting that part of this surplus should be redirected from foreign investments towards domestic European markets, with a particular focus on defence. A large buyer of US Treasuries may therefore gradually scale back.

If you enjoyed this article and found it insightful, subscribe for free below.

With TACO you never know what will happen! Great analysis and good to have in the back pocket.