Beating the Herd: Sizing Your Trades

Most investors focus on whether they're right. Fewer ask how much to bet on it. What blackjack and poker can teach us about probability and position sizing in markets.

Las Vegas, 1961. Ed Thorp sits down at a blackjack table with something no other player has: a proven mathematical edge. While others play on instinct, Thorp is counting, tracking every card dealt and watching the composition of the remaining deck change in real time. When the count tells him the deck is loaded with high cards, he knows that the odds have tilted in his favour. Most players in his position would place an aggressive bet. Thorp, on the other hand, bets a precise fraction of his stake, calculated to maximise his long-run winnings without risking everything.

The Kelly criterion was developed in 1956 by John Larry Kelly Jr. at Bell Labs. Kelly noticed that the mathematics of optimal signal transmission over noisy channels was structurally identical to the mathematics of optimal betting. The result was a formula for bet sizing that maximises long-run growth. If you have an edge, bet a fraction of your stake equal to that edge divided by the odds. Bet less and you leave growth on the table. Bet more and you go broke. Overbet a winning strategy and you reduce long-run growth.

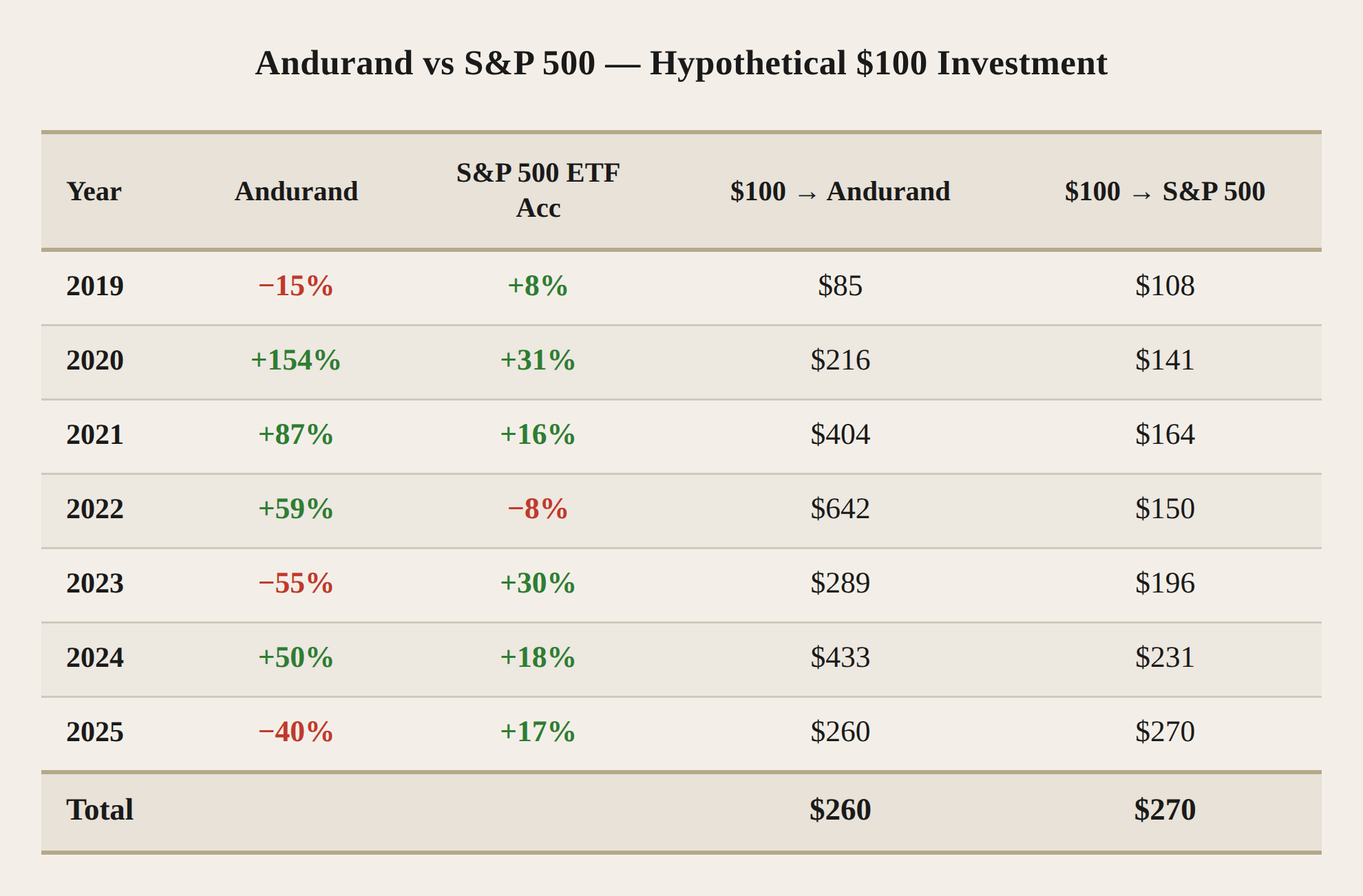

When you decide on the size of your bet, you are making two decisions at once. You are deciding how much you stand to gain if you are right (growth decision), and you are deciding how big of a loss you take if you are wrong (survival decision). Losses and gains are asymmetric, so the recovery from a large loss requires a disproportionate gain just to get back to where you started. For example, if you lose 50% of your capital then you need a 100% return just to break even. Kelly formalises this by optimising for long-run growth rather than single-bet returns. Pierre Andurand’s fund illustrates this precisely: the -55% drawdown in 2023 nearly erased two years of exceptional returns (see table below). Over the full period, the S&P 500 marginally outperformed, but with materially lower volatility.

Sitting sober at the blackjack table, Thorp understood something: the Kelly criterion was not only a gambling tool. It was a framework for any decision made under uncertainty with an identifiable edge. In 1962 he published Beat the Dealer, the first rigorous account of how probability and position sizing could beat a casino. In 1969 he founded what became Princeton Newport Partners, one of the first quantitative hedge funds, applying the same logic to markets. The fund returned 18.2% annually after fees over nearly two decades, without a single losing quarter.

The book reached well beyond the gambling community. Bill Gross, then a psychology student at Duke University, read it and went to Las Vegas to test the theory. He turned $200 into $10,000 over a single summer, sizing his bets in strict proportion to his edge. In 1971 he co-founded PIMCO, which grew into the world’s largest bond fund. He ran it the same way he had run his blackjack stake. “Here at PIMCO it doesn’t matter how much you have, whether it’s $200 or $1 trillion,” he said. “Professional blackjack is being played in this trading room from the standpoint of risk management and that is a big part of our success.”

In practice, applying Kelly to markets is harder. In markets, investors rarely know their true probability of profiting from a trade, and conviction tends to inflate that estimate. Even when applied correctly, uncertain inputs make overbetting the default risk. Additionally, a portfolio built entirely on Kelly’s criterion may be subject to high levels of volatility which oftentimes hurts a fund manager’s credibility. While Kelly is designed to prevent you from going bust, short term periods of large losses are still consistent with a winning strategy. Thorp knew these caveats and typically applied half to three-quarters Kelly in practice. Most hedge fund managers today follow the same logic: those who use Kelly typically apply a fractional version.

The overlap between markets and probabilistic thinking extends well beyond Kelly: Steve Cohen, founder of hedge fund Point 72, has credited poker with teaching him to take risks, and Annie Duke, a World Series of Poker champion, now consults for hedge funds on decision-making under uncertainty.

The question Thorp was asking at that blackjack table in 1961 was not whether he had an edge. He knew he did. The question was how much to bet on it. That question led to a book, a hedge fund, and an inspiration to a generation of fund managers. It is also a question most people almost never ask, in markets or anywhere else. The instinct is often to focus on whether you are right, rarely on how much to bet that you are right.

If you enjoyed this article and found it insightful, subscribe for free below.

Hi! I just saw this post, and thought that it would be a good idea to connect with you. I write about trading, specifically SPY and VIX. Even though this is not exactly my niche, I would appreciate some support, and maybe even a sub! This is one of my latest posts, just for reference. Thanks!

Great reminder that investing isn’t just about being right, but about sizing correctly when you are.